Stakeholder Pensions were introduced in April 2001 and share the same tax advantages as Personal Pensions but contain some specific rules laid down by the Government to ensure that they offer good value particularly for the lower paid.

The main rules are:

- Management charges can’t be more than 1.5% of the fund’s value for the first 10 years and 1% after that

- An investor must be able to start and stop payments at leisure and be able to switch providers without being charged

- Must meet certain security standards, e.g. have independent trustees and auditors

A stakeholder pension allows investors to make contributions of up to £3,600 gross per annum without reference to earnings, or up to 100% of earnings, but subject to the annual allowance, currently £60,000.

The advantage of stakeholder pensions are their relative simplicity, low and capped charges and their availability to almost anyone wanting to establish a pension for either themselves a family member (e.g. a child) or an employee.

Tax Relief on Contributions

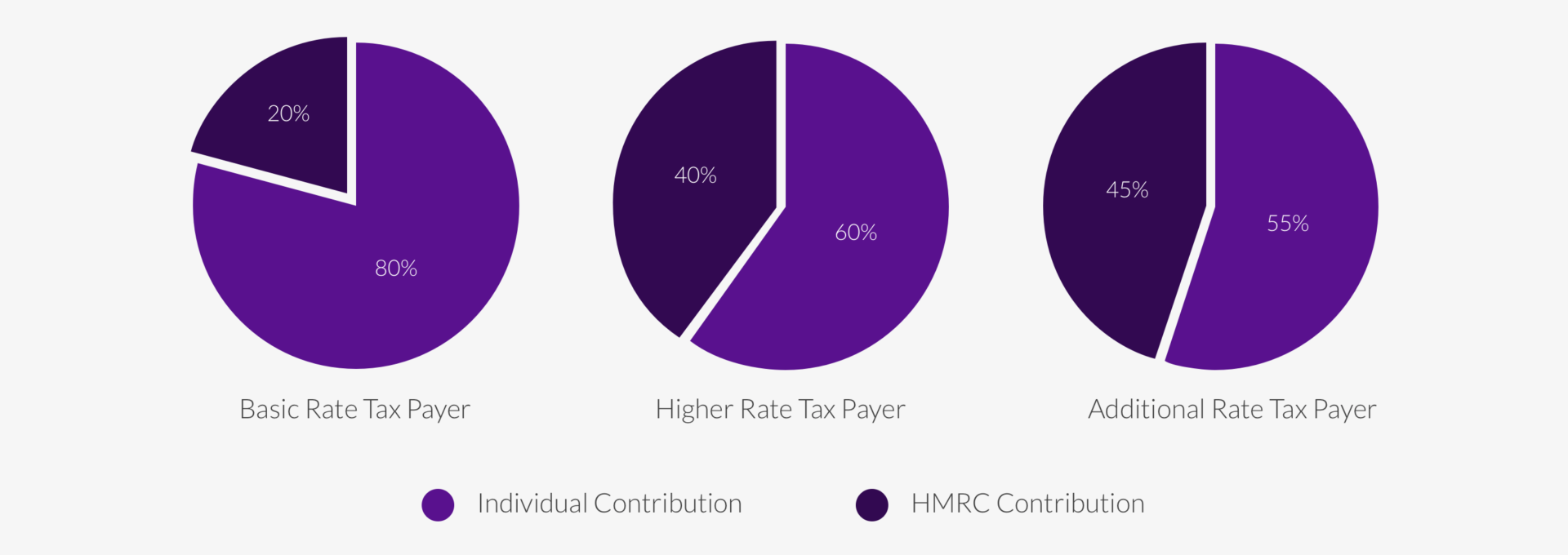

Contributions into a stakeholder pension benefit from an HMRC top-up/rebate of £20 on each £100 paid in by basic taxpayers and £40 or £45 for higher and additional rate taxpayers (reclaimable via a tax return) making these vehicles one of the most tax efficient savings schemes in the UK.

Contributions may be by lump sum or regular payments, paid by the individual, someone on their behalf, or their employer up to their permitted maximum allowance. Employer contributions do not attract National Insurance and qualify for Corporation Tax Relief.

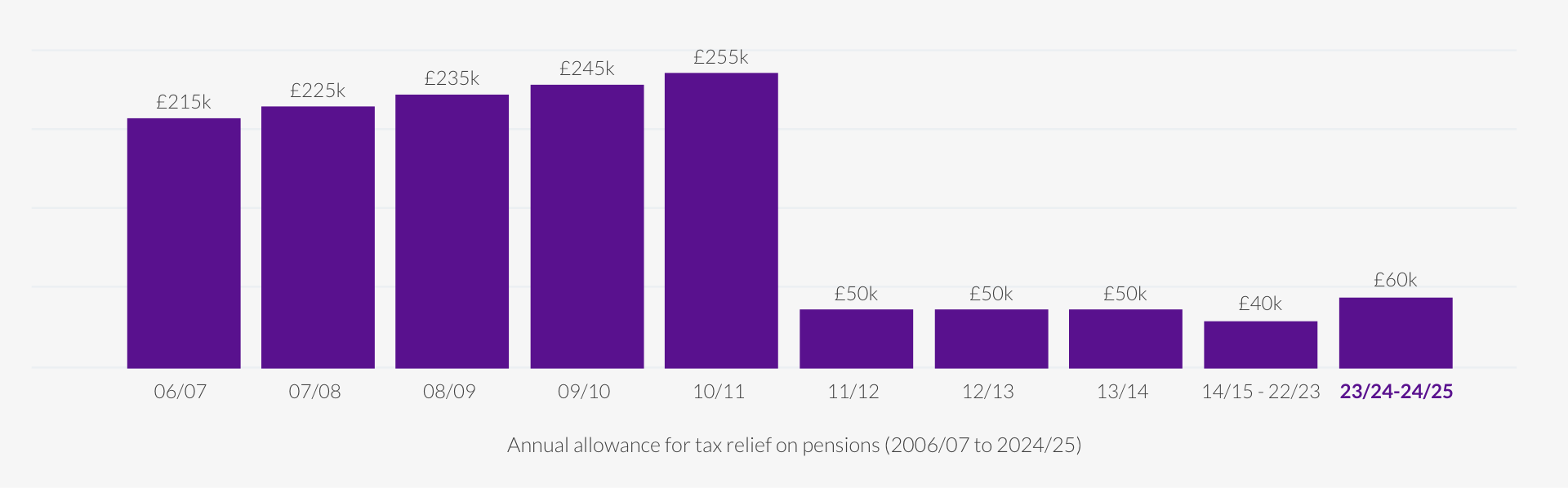

Annual Allowance

There’s a limit to the amount that can be invested in pension plans every year before an individual is taxed on the contributions. It’s set by the Government and it’s called the ‘Annual Allowance’

The current annual allowance is £60,000 pa.

If you are close to contributing up to the allowable limit it would be wise to seek advice from Rosan Helmsley to ensure the limit isn’t breached, which otherwise may trigger a tax charge. Also due to the way contributions are paid to pensions it is important to check the ‘Pension Input Period’ (PIP) to ensure contributions are maximised and allocated in the most tax efficient way.

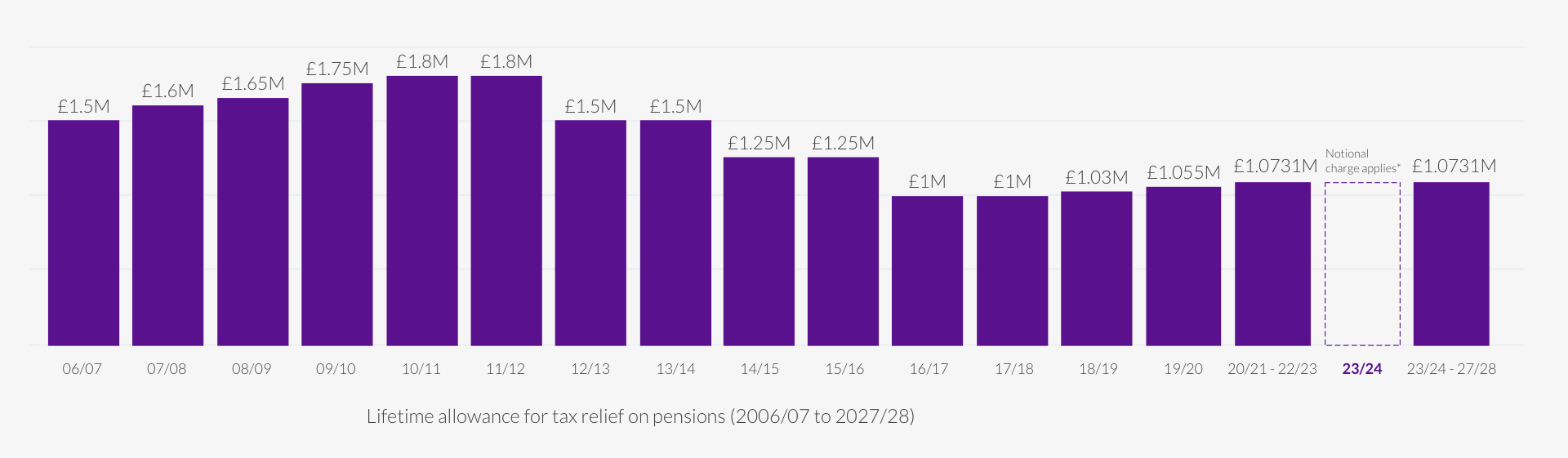

Lifetime Allowance

The Lifetime Allowance (LTA) was abolished from 6th April 2024 and replaced by the Lump Sum Death Benefits Allowance (LSDBA). The standard LSDBA is £1,073,100 matching the former LTA standard cap. Individuals who had transitional protection under the former LTA rules, have a LSDBA greater than £1,073,100 matching their protected higher LTA. The LSDBA is expected to be frozen until 5th April 2028.