Self Invested Pensions

SIPPs (Self Invested Personal Pensions) are one of the most tax efficient methods of making provision for income in retirement. SIPPs have a range and flexibility of investment that makes them particularly attractive to those who wish to actively manage their pension investments.

A Self Invested Personal Pension (a specialist form of personal pension) is one of the most tax efficient ways of saving for retirement.

Unlike most forms of personal pension, a SIPP is independent of the investments it holds. This structure provides a range and flexibility of investment that makes a SIPP one of the most flexible methods of saving for retirement.

Flexible Investment

SIPPs can provide access to a far wider range of investments than a typical Stakeholder or Personal Pension. This enables the structure and risk profile of the underlying investments to be managed over time to suit individual circumstances.

SIPPs can include some of the more well-known types of investments as follows:

- Collective Investment Funds

- Unit Trusts

- Investment Trusts

- OEICs (Open Ended Investment Companies)

- ETFs (Exchange Traded Funds)

- VCTs (Venture Capital Trusts)

- Insurance company managed funds and unit linked funds

- Stocks and Shares

- Individual UK, European, and US equities on recognised stock exchanges

- Gilts, corporate bonds, and other fixed interest securities

- Futures and options

- PIBs (Permanent Interest Bearing shares)/li>

- CFDs (Contracts For Differences)

- Other Investments

- Cash deposit accounts

- Certain National Savings & Investments (NS&I) products

- Commercial property, land, and REITs (Real Estate Investment Trusts)

Tax Free Growth

Investments within a SIPP will accumulate free of any liability to UK income tax or capital gains tax, although tax deducted at source on dividends from equities can no longer be reclaimed.

Tax Relief on Contributions

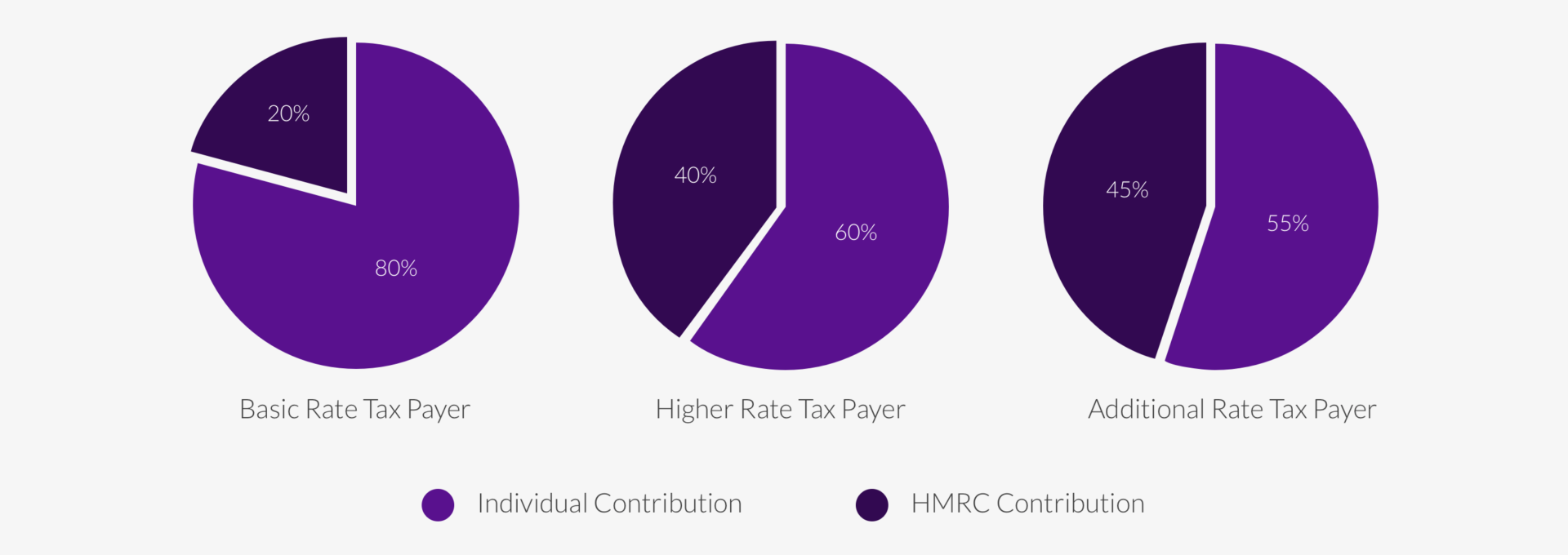

SIPPs enjoy all the tax advantages of a personal pension scheme, receiving tax relief at an individual’s highest marginal rate. Basic rate tax relief is available at 20% immediately and higher rate and additional rate tax payers will need to reclaim the remaining 20% or 25% via their tax return.

Contributions may be occasional lump sums or regular payments, paid by the individual, someone on their behalf, or their employer up to their permitted maximum allowance. Employer contributions do not attract National Insurance and qualify for Corporation Tax Relief.

Contributions can attract tax relief up to 100% of earnings per annum, subject to an annual limit of £60,000, though tapering relief has reduced the amount that high earners can claim tax relief on. For those earning £360,000, or more, per annum tax relief is only available on £10,000 pa of contributions. See our attached Key Guide – Pensions Tax Planning for High Earners.

Annual Allowance

There’s a limit to the amount that can be invested in pension plans every year before an individual is taxed on the contributions. It’s set by the Government and it’s called the ‘Annual Allowance’

The current annual allowance is £60,000 pa.

If you are close to contributing up to the allowable limit it would be wise to seek advice from Rosan Helmsley to ensure the limit isn’t breached, which otherwise may trigger a tax charge. Also due to the way contributions are paid to pensions it is important to check the ‘Pension Input Period’ (PIP) to ensure contributions are maximised and allocated in the most tax efficient way.

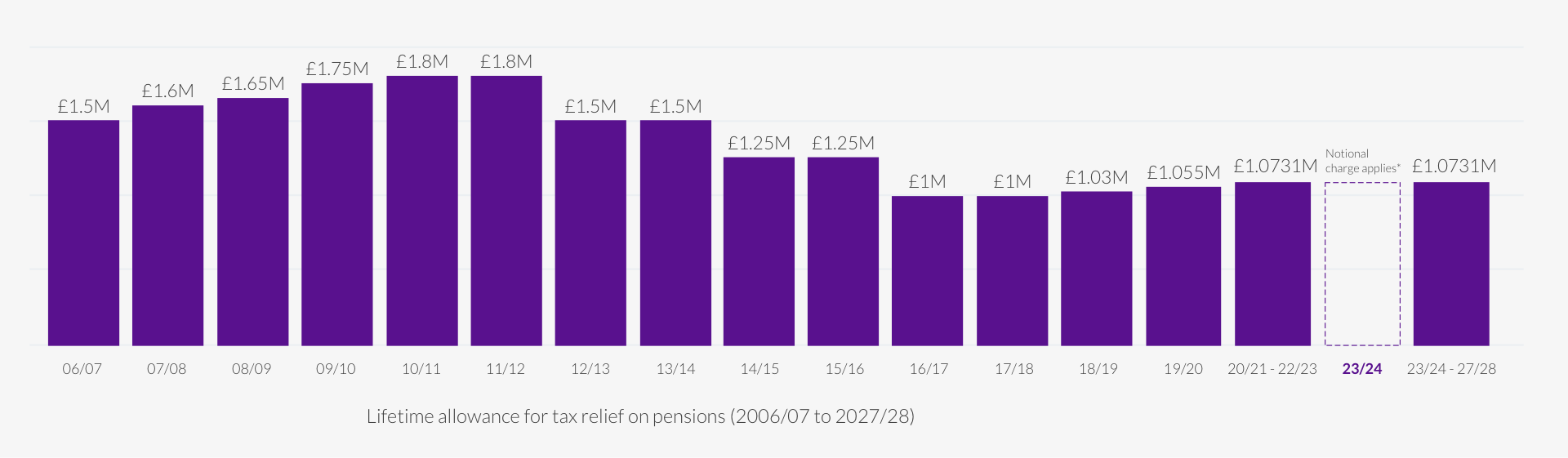

Lifetime Allowance

The Lifetime Allowance (LTA) was abolished from 6th April 2024 and replaced by the Lump Sum Death Benefits Allowance (LSDBA). The standard LSDBA is £1,073,100 matching the former LTA standard cap. Individuals who had transitional protection under the former LTA rules, have a LSDBA greater than £1,073,100 matching their protected higher LTA. The LSDBA is expected to be frozen until 5th April 2028.

Pension Consolidation

For those who have accumulated a number of pension schemes throughout their career, a consolidation in to a SIPP can have significant attractions, as this will generally allow for a much more consolidated investment strategy and of course, simpler administration.

For those who have deferred pension benefits in a defined benefit scheme, the pension freedom legislation has allowed an opportunity for potentially bringing these assets into the SIPP structure. This is a highly specialised area of financial planning advice, and only those with the relevant qualifications can give guidance under this heading.

If you are considering deferred defined benefit pensions, this is an area that requires very specific financial advice, and Rosan Helmsley advisors are trained in this complex area.

The advice is so specialised that the FCA have determined that individuals transferring defined benefit pensions over a certain limit have to seek specialist financial advice before a transfer can be made.

This is essentially because defined benefit schemes provide inherent guarantees and rightly the government is concerned about those transferring benefits without giving thought to the consequences if the investments go wrong under a self-invested structure.

If you wish to discuss potentially consolidating deferred defined benefit pensions, then please do contact our office.

Flexible Income

SIPPs offer the widest range of retirement options, 25% of the fund may be taken as a tax free lump sum from the age of 55. The remaining funds are used to provide income in retirement, which is taxable. How an individual elects to draw their retirement income is now very flexible and includes options such as annuity purchase, income withdrawal, income drawdown and phased income drawdown.

Eligibility

SIPPs offer the widest range of retirement options, 25% of the fund may be taken as a tax free lump sum from the age of 55. The remaining funds are used to provide income in retirement, which is taxable. How an individual elects to draw their retirement income is now very flexible and includes options such as annuity purchase, income withdrawal, income drawdown and phased income drawdown.

Contact us for further information.